5 min read

Once you start reading more about investing, you’ll encounter an array of acronyms, with two of the most common being DCA (dollar cost averaging) and LS (lump-sum) investing. DCA is an investment strategy where an investor makes regular purchases of a fixed amount of money over time regardless of the price, while LS entails investing a significant portion of the funds all at once. There’s much debate over which approach yields better future returns and which one prudent investors should opt for.

If you’ve also encountered this dilemma and begun researching online, you’ve likely come across arguments in favor of LS investing over DCA, citing the saying that “time in the market is more important than timing the market.” However, many of these analyses overlook a crucial aspect: the size of the lump-sum investment. If you’re considering investing a substantial amount of money in one go (e.g. your full investment budget of lifetime), especially with a long-term investment horizon, it may indeed make sense to do so as soon as possible, benefiting from more time in the market. However, not everyone has the luxury of a sizable lump sum readily available for investment. Many individuals rely on their regular income to make smaller monthly purchases or invest their yearly bonuses, making the these analyses less relevant for them.

For these investors, the critical question is whether to invest their bonuses (or part of their salary) whenever they receive them or opt for regular monthly purchases instead. When we analyze the results within this context, the findings are quite intriguing.

Simulation Details:

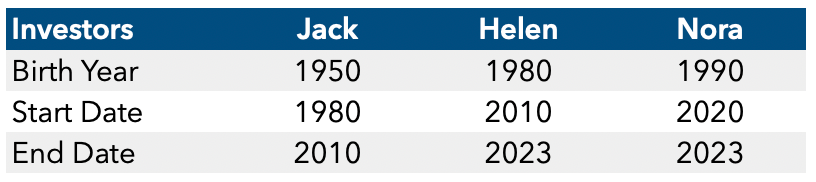

In our simulation, we consider three investors: Jack, Helen, and Nora.

- Jack, a baby boomer born in 1950, begins his investment journey in 1980 at the age of 30, investing $10,000 yearly and adjusting this amount annually for inflation until his retirement 30 years later in 2010.

- Helen, one of the last Gen Xers born in 1980, starts her investments in 2010, investing $28,000 yearly and also adjusting it annually for inflation.

- Nora, a millennial born in 1990, follows a similar strategy, beginning her investments at 30 years old in 2020 with $12,000 per year.

Our simulation methodology involves implementing DCA with monthly investments at a fixed amount (the inflation-adjusted yearly budget divided by 12) and LS with a single investment simulated for each calendar month to account for seasonality. We utilize S&P 500 index data to simulate investment earnings, while uninvested DCA amounts are kept in a cash account without earning interest.

Findings:

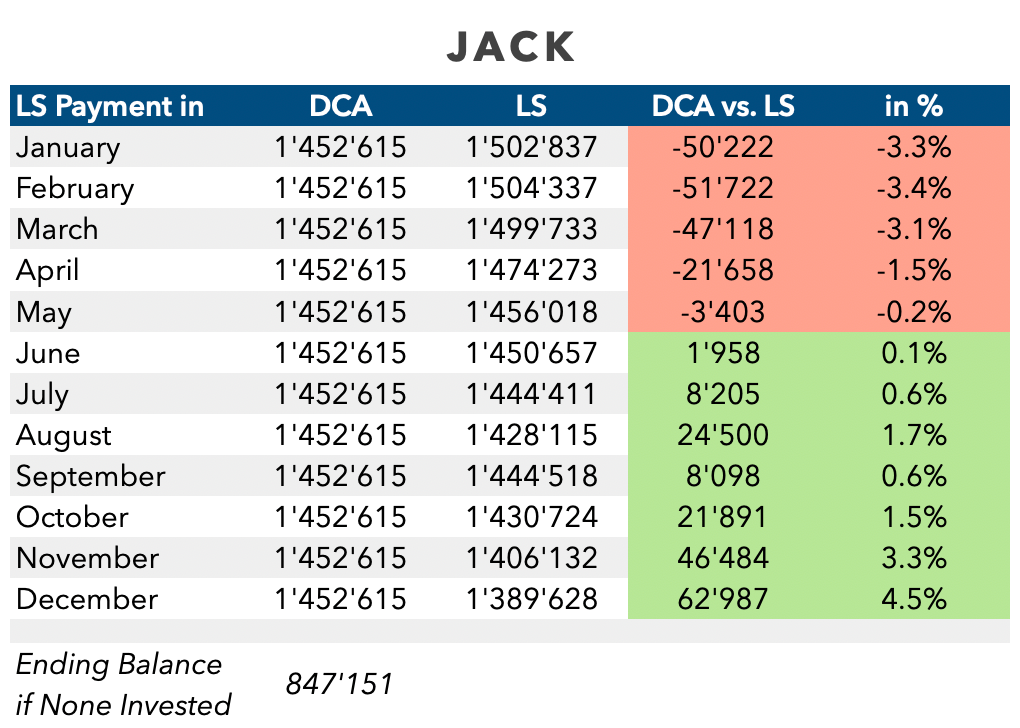

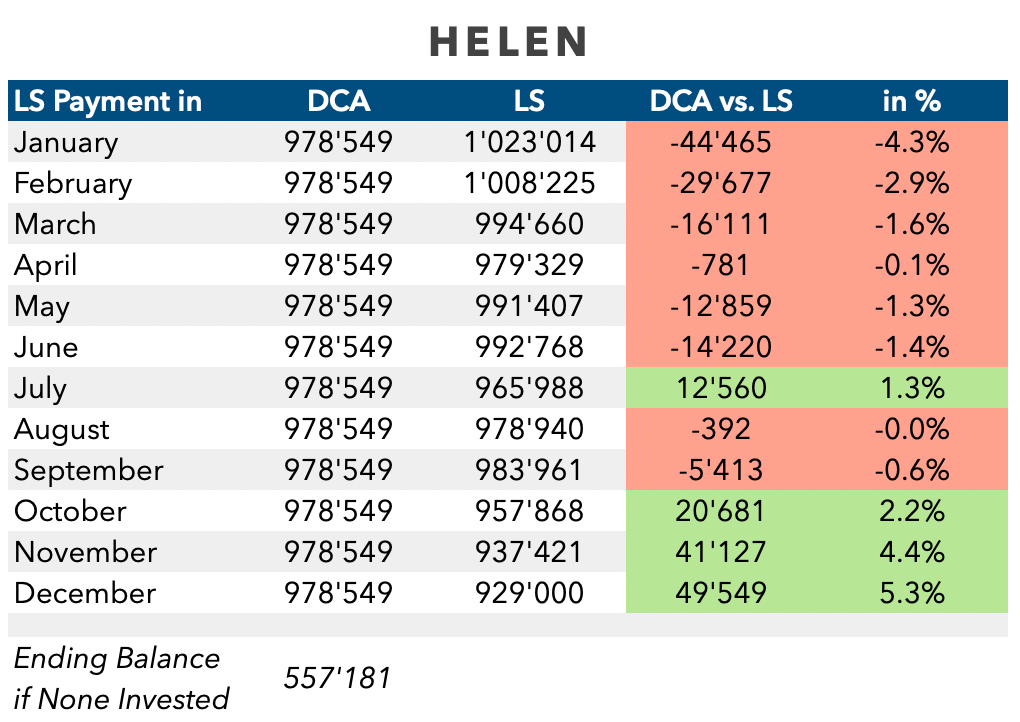

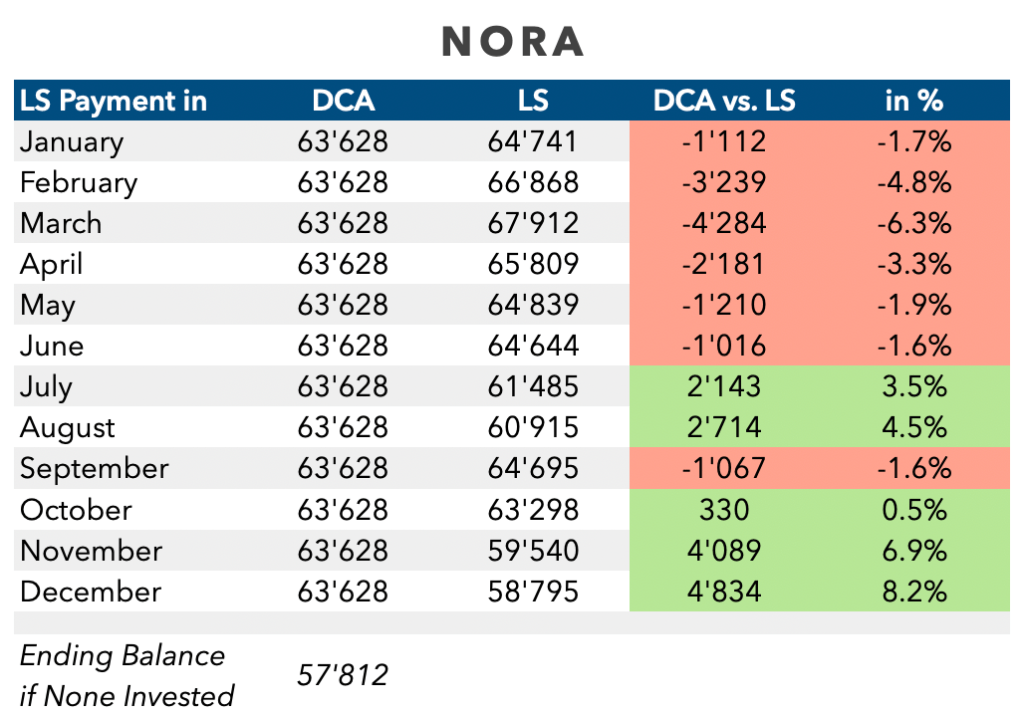

Let’s check the results. In each table below (one for each investor), you’ll see the value of their investments at either their retirement age (2010 for Jack) or the most recent year (2023 for Helen and Nora).

Jack’s investments are worth over $1.4 million, nearly double what he would have had if he hadn’t invested and instead kept his funds in a savings account earning interest at the inflation rate. When comparing DCA to LS, DCA proves to be more profitable in 7 out of 12 months. However, the percentage difference between LS and DCA is not significant, although the dollar amount may vary depending on the invested sum. Another intriguing finding is that making LS investments at the beginning of the year tends to yield more profit compared to doing so at the end of the year. Let’s see if this pattern holds true for the other investors as well.

Helen also enjoys substantial profits compared to a savings account, but now LS investments proving more profitable in more months. Again, the percentage difference remains small, and LS investments at the beginning of the year are more advantageous.

Nora also benefits from her investments, with LS investments being more profitable in most months same as Helen. However, the percentage difference becomes more pronounced as her investment horizon is shorter in this example. As years pass, we expect both DCA and LS to yield more similar results to Jack’s.

Learnings:

While past returns are not indicative of future performance, deriving insights from historical data remains valuable. As long as economic growth trends upward in the long term and adds value to the system, similar outcomes may occur in the future. Therefore, investing for the long term is advisable for maintaining or increasing living standards. Regarding DCA and LS, as demonstrated in the examples above, there may be a slight difference in the short to medium term when there’s an upward trend with volatility, but in the long term, the difference is negligible (with DCA marginally outperforming LS). Additionally, this simulation assumes that uninvested amounts in DCA scenarios do not earn interest, so including this factor may make DCA slightly more favorable. However, if one wishes to do LS investing, then doing it at the beginning of the year (or as early as possible) make sense, as markets tend to be on an upward trend, and investing in January (assuming one receives yearly bonus at that time) allows for more time in the market.

Is LS essentially a longer-term form of DCA?

For our simulated investors, the answer is yes. Since they make LS investments annually, it essentially functions as DCA with a wider purchasing horizon (yearly instead of monthly).

Given these findings, I personally prefer to follow monthly DCA as it is less emotionally stressful and potentially allows for adjustment of investment amounts in response to significant price movements. If I were to make all my yearly purchases at once, I might miss out on these opportunities. Ultimately, you should choose the approach that makes you most comfortable and allows you to sleep soundly at night, free from worries about market timing.

Leave a comment