4 min read

This week’s post is a literature review discussing the topic of dividends, which are payments made by companies to their shareholders from their profits, typically on a regular basis.

Many investors favor receiving dividends and thus invest in high dividend yield (HDY) companies. For them, it’s a reliable income source without reducing their capital, akin to receiving a salary or interest. For others, dividends aren’t as straightforward, coming with both direct (e.g., stock price decreases) and indirect costs (e.g., taxes, cost of reinvesting). They may opt for no dividend (ND) or low dividend yield (LDY) companies.

Let’s analyze some academic papers to explore this further.

Over 60 years ago, Miller and Modigliani (1961) argued that investor characteristics influence dividend stock selection, with tax-exempt institutional investors and retail investors with low marginal tax rates likely to prefer high dividend yield (HDY) stocks. Shefrin and Thaler (1981, 1988) show that older investors may prefer HDY as they may use dividend income to finance consumption and prefer cash dividend over self-made dividends (i.e., income generated by the partial liquidation of the portfolio), while younger investors tend to prefer low dividend yield (LDY) stocks. In 2006, Graham and Kumar found out (based on studying the stock holdings of more than 60,000 households) that a preference for HDY increases with age (consistent with life cycle or consumption preferences) and decreases with income (consistent with low tax investors holding HDY stocks).

In a more recent paper, Hartzmark and Solomon (2018) investigated some of the behavioral reasons for dividend preference. As money is fungible, receiving $1 worth of dividend (with the stock price declining by the same amount) and selling $1 worth of that stock should be equal for an investor. However, in reality, people are not indifferent. Hartzmark and Solomon call this phenomenon the free dividends fallacy as people perceive dividends as a free source of income. Dividends are often viewed as a hedge against market fluctuations, ignoring the fact that they come at the expense of the stock’s price level.

Dividends cause the stock price to decrease (some investors argue that this doesn’t always happen, but it’s important to note that while, on average, share prices decrease in line with dividends, market movements play a larger role in daily stock price fluctuations, making this effect less visible). Additionally, dividends create a tax burden for private retail investors, like us (this varies by country, but in Switzerland, for example, capital gains are not taxed, whereas dividends are), as well as trading costs for reinvestment (which is maybe the best possible use-case of dividends). Moreover, when a company pays out cash dividends, it foregoes potential growth opportunities by not reinvesting that cash in itself (though companies may take alternative actions, such as stock buybacks, which also benefit shareholders but don’t always contribute to their growth).

Hartzmark and Solomon (2018) also discovered that dividend-paying stocks are traded less frequently (investors who place a high value on dividend payments may be less reactive to price fluctuations), and financial analysts tend to be overly optimistic in their forecasts of future prices. Additionally, even sophisticated investors seldom reinvest dividends back into the asset from which they originated.

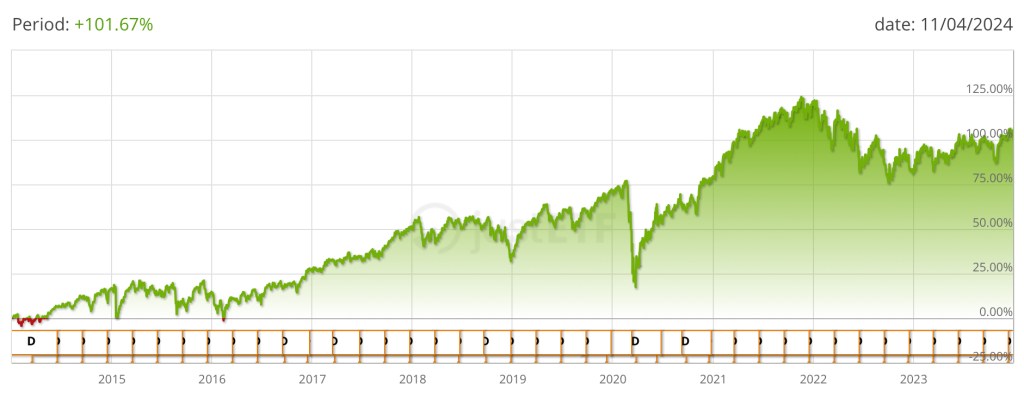

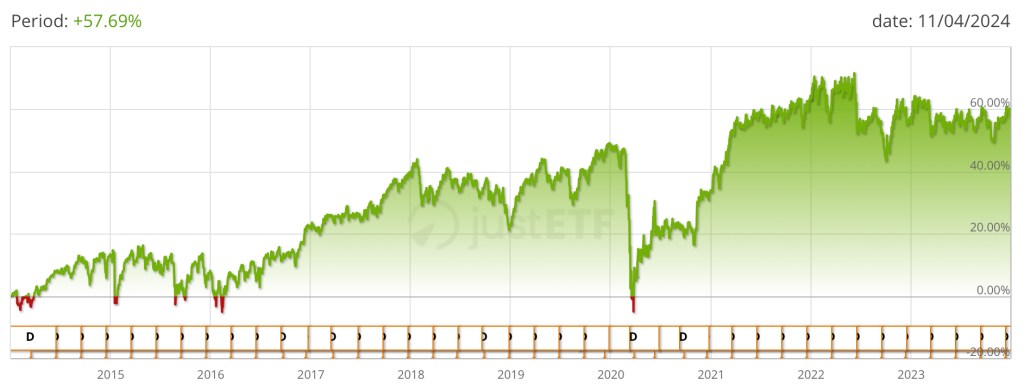

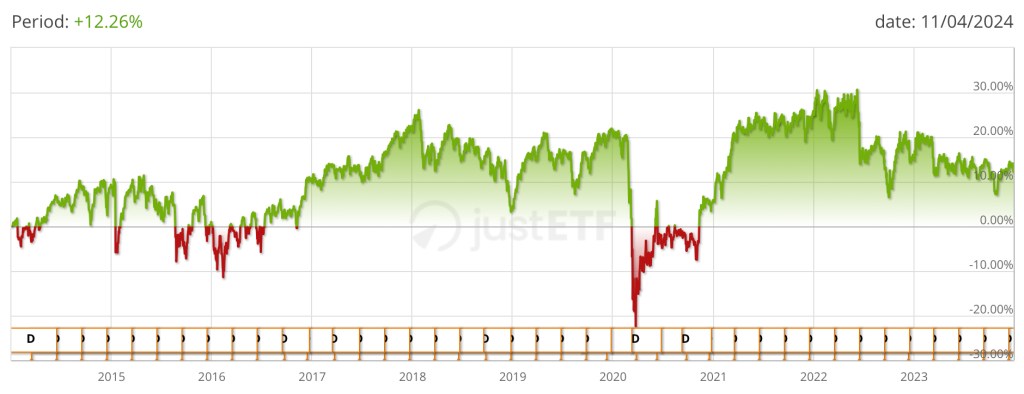

I was also curious to see how high dividend yield (HDY) paying stocks are performing in the market. So, I compared two major ETFs from Vanguard: one is globally diversified (VWRL, IE00B3RBWM25) and the other is also globally diversified, but with HDY stock preference (VGWD, IE00B8GKDB10). I used the justetf.com website to compare both funds’ performance, considering dividends in the calculation (dividends are virtually reinvested at the ex-date). As seen from the results below, over the past 10 years, VWRL has outperformed VGWD both with and without dividends accounted for. This suggests that companies paying high dividends do not necessarily perform better in the stock market.

Given all these findings and my belief in leveraging academic knowledge, which is based on historical facts and statistical analyses, in my investing strategy, I am part of the investor group who opts for low dividend yield companies/ETFs.

References:

Miller, M. H., & Modigliani, F. (1961). Dividend Policy, Growth, and the Valuation of Shares. The Journal of Business, 34(4), 411–433. http://www.jstor.org/stable/2351143

Thaler, Richard H., & Hersh M. Shefrin. (1981). An economic theory of self-control. Journal of Political Economy, 89, 392-406. https://doi.org/10.1086/260971

Shefrin, Hersh M., & Richard H. Thaler. (1988). The behavioral life-cycle hypothesis,. Economic Inquiry, 26, 609-643. https://doi.org/10.1111/j.1465-7295.1988.tb01520.x

Graham, J. R., & Kumar, A. (2006). Do Dividend Clienteles Exist? Evidence on Dividend Preferences of Retail Investors. The Journal of Finance, 61(3), 1305–1336. http://www.jstor.org/stable/3699324

Leave a comment